IRS Taxes Kentucky Derby Wins, But Can You Deduct Losses?

$5,000 Welcome Bonus

Rich Strike’s improbable Kentucky Derby win made the owner flush, with a $1.86M purse on a horse that only cost $30,000. There were plenty of other winners too, for anyone bold and prescient enough to take a flier bet on this most unlikely of winners at Churchill Downs. The most amazing type of win would have been the so-called superfecta bet. To win that one, you had to correctly predict not only Rich Strike as the winner, but also pick the second, third and fourth place finishers of the Derby. This year, that was Epicenter (4-1), Zandon (6-1) and Simplification (35-1), respectively. The payoff if you did and on a $1 bet would have been $321,500.10. But there were plenty of big payoffs just for doing the improbable: betting on a horse with 80 to 1 odds.

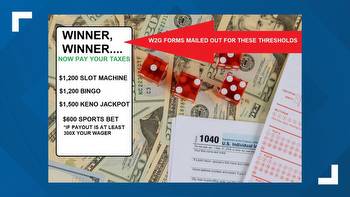

How much does the IRS collect? 37%, just like other income—although the Biden administration is proposed raising the top rate up to 39.6%. The IRS has some useful but sobering missives about gambling winnings. There’s this leaflet, You Won! from the IRS, and if you want to read a lot more, there’s an IRS publication on gambling income and losses. You must report the full amount of your gambling winnings for the year on your Form 1040. Of course, may could get a nice reminder. Depending on the type and amount of your winnings, the payer might provide you with a Form W-2G, a special form for reporting certain gambling winnings. They may even withhold federal income taxes from the payment. But even if they don’t, you still have to report and pay tax. There is information on withholding on gambling winnings in IRS Publication 505.

Of course, any time there are big winners, there are big losers, and the Kentucky Derby had many this year, especially when you think about all those favorites that seemed like sure things. After the race, nothing seemed certain about all those likely winners. So what about the tax treatment of all those losses? That is one of the things gamblers find must annoying. You might think you can just net your wins and losses, but the IRS doesn’t permit that. You may deduct gambling losses only if you itemize your deductions on Schedule A (Form 1040 or 1040-SR) (PDF) and kept a record of your winnings and losses. The amount of losses you deduct can't be more than the amount of gambling income you reported on your return. Claim your gambling losses up to the amount of winnings, as Other Itemized Deductions. Of course, with the new tax rules that took effect starting in 2018, it is harder to itemize now.

It is important to keep an accurate diary or similar record of your gambling winnings and losses. To deduct your losses, you must be able to provide receipts, tickets, statements or other records that show the amount of both your winnings and losses. Sadly, this is why most people are not able to claim their losses. The IRS wants you to keep quite a lot. Just look at the list. Keep the date and type of your specific wager or wagering activity. The name and address or location of the gambling establishment. The names of other persons present with you at the gambling establishment. The amount(s) you won or lost. If you don’t keep extremely good records, you may end up losing out again when it comes to the IRS.