LVS: 3 Casino Stocks to Avoid as Macau Announces Increased Government Supervision

$5,000 Welcome Bonus

The casino industry has experienced a decent recovery this year with the reopening of brick-and-mortar casinos and the growing popularity of online gambling. However, shares of Macau casino operators declined by approximately one-third of their values, losing about $18 billion, on September 15, as Macau declared stronger supervision of casino companies in the world’s largest gambling hub. Macau’s secretary for economy and finance, Lei Wai Nong, gave notice of a 45-day consultation period, pointing to shortcomings in the industry’s supervision.

The new regulations are designed primarily to restrict illegal cash transfers and unregulated lending. However, the shares of U.S. operators suffered the worst selloffs on investor anxiety over the uncertainty surrounding the future of casinos in Macau.

Given this backdrop, we think it could be wise to steer clear of casino stocks Las Vegas Sands Corp. (LVS), MGM Resorts International (MGM), and Wynn Resorts, Limited (WYNN), which possess weak growth prospects and bleak financials.

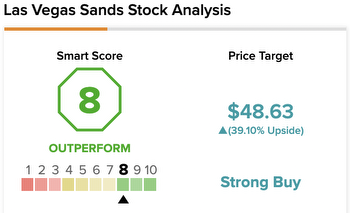

Las Vegas Sands Corp. (LVS)

LVS develops and operates integrated resorts and focuses on leisure tourism with eight properties across the U.S. and Asia. The resorts feature accommodations, gaming, entertainment, retail malls, convention and exhibition facilities, celebrity chef restaurants, and other amenities.

This month, LVS’ majority-owned subsidiary priced $700 million in 2.3% senior notes due 2027, $650 million in 2.85% senior notes due 2029, and $600 million in 3.25% senior notes due 2031. Sands China intends to use the net proceeds of approximately $1.93 billion from the offering to repay its outstanding $$1.80 billion 4.6% senior notes due 2023.

In March, LVS entered definitive agreements to sell its Las Vegas real property and operations, including The Venetian Resort Las Vegas and the Sands Expo Center, for around $6.25 billion. This could negatively affect the company’s revenues in the near term.

LVS’ operating expenses under resort operations increased 89.4% year-over-year to $932 million in the second quarter, ended June 30, 2021. The company’s interest income declined 75% from its year-ago value to $1 million. In addition, LVS’ operating loss came in at $139 million, while its net loss amounted to $242 million during this period.

LVS’ EPS is expected to decrease at a 6.3% rate per annum over the next five years. The company’s consensus EPS is expected to remain negative in the fiscal period ending December 2021. Moreover, the stock has lost 42.1% in price over the past six months.

LVS’ POWR Ratings are consistent with this bleak outlook. The stock has an overall D rating, which equates to a Sell in our proprietary rating system. The POWR Ratings assess stocks by 118 different factors, each with its own weighting.

Also, the stock has a D grade for Value, Stability, and Sentiment. We’ve also graded LVS for Growth, Quality, and Momentum. to access all of LVS’ ratings. LVS is ranked #25 of the 32 stocks in the C-rated Entertainment – Casinos/Gambling industry.

MGM Resorts International (MGM)

Along with its subsidiaries, MGM owns and operates casino, hotel, and entertainment resorts in the United States and Macau. Las Vegas Strip Resorts; Regional Operations; and MGM China are the company’s three operational segments. Its portfolio consisted of 29 hotel and destination gaming services as of February 17, 2021.

For the second quarter, ended June 30, 2021, MGM’s operating expenses grew 58.6% from the year-ago value to $2.09 billion. Also, the company’s expenses under its casino segment increased 207.8% year-over-year to $616.9 million. Its negative adjusted EBITDAR under the corporate segment rose 13.8% from the prior-year quarter to $90.27 million. In addition, MGM’s net loss came in at $14.45 million during this period.

MGM’s EPS is expected to remain negative in its fiscal period ending December 2021. In addition, analysts expect its EPS to decline at a 129.2% rate per annum over the next five years. The stock’s price has retreated 1.8% over the past five days.

MGM’s poor prospects are also apparent in its POWR Ratings. The stock has a D grade for Stability. MGM is ranked #17 of 32 stocks in theEntertainment – Casinos/Gambling industry.

In addition to the POWR Rating grades I’ve just highlighted, one can see MGM’s ratings for Value, Quality, Growth, Sentiment, and Momentum here.

Wynn Resorts, Limited (WYNN)

Incorporated in 2002, WYNN is a developer and operator of hotels and casinos. The company operates through four segments: Wynn Palace; Wynn Macau; Las Vegas Operations; and Encore Boston Harbor. WYNN’s hotel and casino centers provide the customers a wide range of games, health clubs, spa, pool, salon, and various entertainment features.

For the second quarter, ended June 30, 2021, WYNN’s operating loss came in at $29.52 million. Furthermore, the company’s total operating expenses grew 67.5% from its year-ago value to $1.02 billion. It reported a $173.4 million net loss, while its loss per share came in at $1.15 during this period.

The company has failed to beat the consensus EPS in three of the trailing four quarters. WYNN’s EPS is expected to decline at a 114.9% rate per annum over the next five years. Furthermore, the stock’s price has declined 33.5% over the past three months and 40.5% over the past six months.

It’s no surprise that WYNN has an overall D rating, which equates to a Sell in our POWR Rating system. The stock has a D grade for Value, Stability, and Sentiment.

to see the additional POWR Ratings for WYNN (Momentum, Growth, and Quality). WYNN is ranked #26 in theEntertainment – Casinos/Gambling industry.

LVS shares were trading at $36.98 per share on Monday afternoon, down $1.19 (-3.12%). Year-to-date, LVS has declined -37.95%, versus a 15.67% rise in the benchmark S&P 500 index during the same period.